Paying off your 'closing balance'

The best way to avoid credit card interest is to pay off your closing balance before your statement’s due date.

If you have a balance transfer, you'll need to pay the interest-free days payment shown on your statement.

Your closing balance is the total amount you owe on your credit card when we create your statement at the end of the statement.

If you want to pay off your entire credit card debt for the month, the closing balance is the amount you’ll need to pay.

If you pay this amount by the due date, or if your statement displays an interest-free days payment, you won't be charged any interest on your purchases.

Learn how to read your credit card statement.

Pay more than your monthly minimum repayment

If you can't afford to pay off your credit card in full each month, consider paying a little more than your monthly minimum repayment instead.

By paying a little extra each month, you can pay off your credit card faster and pay less interest. Check out the ASIC Repayment Calculator, opens in new window to see how much you can save by making higher repayments.

The thought of paying that little bit extra can be daunting. A budget might help you stay on top of your expenses and even help you work towards paying off your credit card balance in full.

Learn ways to save and budget successfully.

Use your interest-free period

Most of our credit cards have an interest-free period. Depending on your card, the interest-free period will be up to 44 days or up to 55 days.

To be clear, this doesn’t mean you get 44 or 55 days interest-free from the moment you buy something. The 44 or 55 days begins at the start of your statement period and ends at your statement due date. This is what we mean by 'up to'.

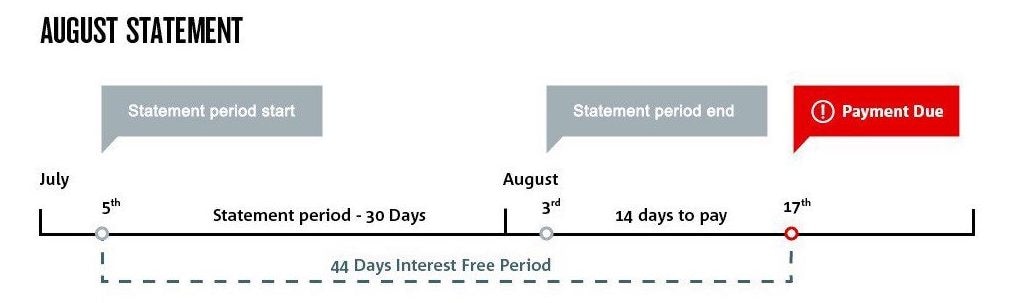

How an interest-free period works

In this example, we're using an August credit card statement. Purchases on this statement would have been made during the statement period in July.

If the statement period begins on July 5, this is also the date that the 44 days interest-free period begins.

If the statement period ends on August 3, you then have 14 days, ending on August 17, as your ‘payment window’ to make a payment.

To avoid paying interest in this example, you would need to pay off the entire closing balance by August 17.

Transactions that don't have an interest-free period

- Cash advances: these are cash withdrawals made from your credit card account.

- Gambling transactions (these are considered cash advances).

- Purchasing traveller’s cheques or gift cards.

- Buying or loading value onto a prepaid or store-value card.

Avoid cash advances if possible

A standard cash advance is withdrawing cash from your credit card. But since this isn't considered a purchase, interest-free days don’t apply. This means interest starts to add up from the moment you make the withdrawal.

Cash advances should be a last resort or in case of an emergency. If you need cash, it’s a way to get it if you’re stuck. But remember, the interest charged for cash is usually quite high, so try to pay it back as soon as possible.

Other cash advance examples include:

- cash out from your credit card account at an ATM, or over the counter

- money transferred out of your credit card and into another account

- using your credit card for gambling

- bills paid with your credit card over the counter at another bank or at a post office (online bill payments are usually okay, but you should check with your biller first)

- traveller’s cheques or gift cards.

Pay attention to special rates

Special rates for purchases end, and the end date isn’t the last day you can make purchases at a special rate. It's the last day we’ll charge you the special rate.

For example. If a special rate ends 31 December, your closing balance will accrue higher interest from 1 January. This is regardless of any purchases before 31 December.

Set up alerts and regular payments

If you think you’re likely to forget to make manual payments, why not set up a direct debit in internet banking or the NAB app to pay it in full each month?

NAB Internet Banking

- Login to NAB Internet Banking (from your desktop).

- Open Accounts and select Account details.

- Select your credit card.

- Click Create or modify Direct Debit.

- Follow the prompts to complete the form.

The NAB app

- Login to the NAB app.

- Open Cards and select your credit card.

- Scroll down to Repayment details.

- Tap Manage automatic payments.

- Follow the prompts to complete the form.

If you’d still prefer to pay it manually, you can set up a payment reminder using NAB Alerts as a prompt.

Learn more about paying your credit card.

Get in touch if you're facing hardship

We understand that life can take unexpected turns and leave you in a vulnerable financial position. If you're finding your credit card repayments difficult to make, we may be able to offer financial hardship assistance.

Explore other life moments

Related products and services

Get in touch

Customer Support Tool

Solve problems quickly online with our easy-to-follow guides. Simply select a topic and we’ll direct you to the information you need.

Contact us

Visit our personal banking contact page for FAQ’s and how-to-guides, help from our virtual assistant and contact numbers.

Visit a NAB branch

Visit us in person at your nearest NAB branch or business banking centre.

Terms and Conditions

Apologies but the Important Information section you are trying to view is not displaying properly at the moment. Please refresh the page or try again later.

Credit cards issued by National Australia Bank Limited. © 2020 National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.

The information contained in this article is intended to be of a general nature only. It has been prepared without taking into account any person’s objectives, financial situation or needs. Before acting on this information, NAB recommends that you consider whether it is appropriate for your circumstances. NAB recommends that you seek independent legal, financial and taxation advice before acting on any information in this article.