Credit reporting and financial hardship arrangements - NAB

What is Comprehensive Credit Reporting (CCR)?

Comprehensive Credit Reporting (also known as a credit report) includes detailed information such as the types of credit accounts you hold (like credit cards, home loans and personal loans), how many you have and whether your repayments are made on time each month.

This information helps lenders, such as banks and utility providers, assess your creditworthiness when you apply for a product or service.

Watch our video to learn more.

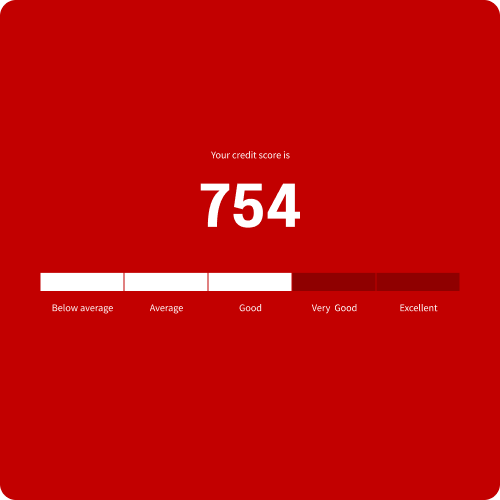

What is a credit score?

Your credit score is a number ranging from 0 to 1200, that summarises the information in your credit report. It reflects your financial history and health and helps lenders understand how likely you are to repay debt.

How to check your credit score

You can request a free copy of your credit report and check your credit score through a credit reporting body. You're entitled to one free report every 3 months, so it's a good idea to review this regularly to make sure the information is accurate.

Equifax Personal

Equifax is a global information and insights company and a leading provider of credit information and analysis in Australia.

Experian Australia

Experian collects and analyses credit information on individuals and businesses to create credit reports and scores.

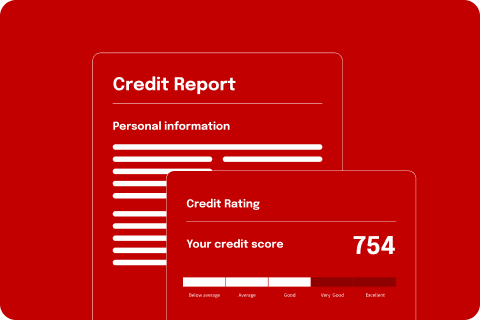

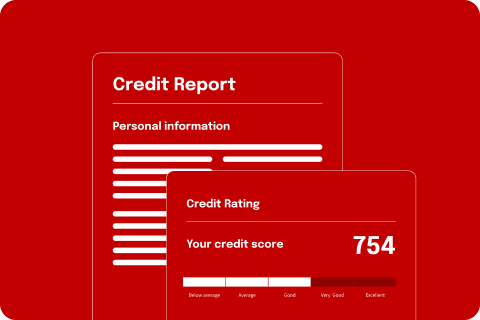

What you’ll find in your credit report

Your credit report includes, but is not limited to, the following information:

- General personal information (such as your name, date of birth and address).

- The types of loan and credit accounts you hold.

- When each account was opened and closed, if applicable.

- The current credit limit on each account.

- Whether your account is part of a financial hardship arrangement or has been permanently varied under a hardship agreement.

- Whether you have missed or made late payments.

How credit reporting works

CreditSmart is an independent and informative resource that helps Australians better understand how credit reporting works including how to access and check your credit report.

Key components that make up your credit report score

What is Repayment History (RHI)?

Repayment History Information (RHI) shows whether you've made your credit repayments on time each month. If you’ve missed a repayment, your credit report will show how many months you’re overdue.

This information stays on your credit report for 24 months. We share your RHI with credit reporting bodies Equifax and Experian every month.

What is financial hardship information (FHI)?

Financial Hardship Information (FHI) appears on your credit report when you’ve entered into a formal hardship arrangement with your lender. It shows that you're taking steps to manage your financial situation and work toward recovery.

Financial Hardship Information stays on your credit report for 12 months.

What is a credit enquiry?

A credit enquiry, also known as a credit check, occurs when a lender (such as a bank) reviews your credit history as part of an application for a product like a loan or credit card. This helps them assess your repayment history and make a decision about whether to approve or decline your application.

Credit enquiries stay on your credit report for five years.

What is a default listing?

A default listing appears on your credit report when you've missed multiple payments on a debt such as a loan or credit card and the lender has formally marked the account as unpaid.

Before this happens, we’ll try to contact you through phone calls, letters and SMS. It’s important to get in touch with us early so we can offer support and help you manage your repayments.

Default listings stay on your credit report for five years.

Missed payments and your credit score

Debt escalation process

Financial assistance for your needs

Support for the products you rely on, when you need it most.

Financial assistance

Needing to reach out for financial assistance can happen to anyone. You’re not alone. We’re here to help. Learn more about our financial assistance.

Home loan financial assistance

If you're finding it hard to make your home loan payments, we’re here to help with support options tailored to your needs.

Credit card and personal loan financial assistance

If you’re having trouble keeping up with your payments on your credit card, personal loan or NAB Now Pay Later products, we’re here to help.

Business financial assistance

If your business is under financial pressure, we have support options to help you through.

Extra support when you need it

We understand that life can be challenging sometimes. That’s why we offer support for a range of situations.

Natural disaster support

Support before, during and after a natural disaster.

Domestic and family violence support

Safe and confidential help if you’re experiencing violence at home.

Financial abuse and elder financial abuse support

Support if someone is using money to harm or control you.

Unplanned life moments

Sometimes things don’t go to plan. Divorce, illness or job loss can be unexpected. Here are some tools and guides to help.

Gambling support

Help to take back control of your gambling spending.

Customer Care Kit

Explore our comprehensive guide to community support services available to you.

Accessible help for everyone

We offer a range of accessible services to help you access the right support, in the way that works best for you.

External support

Access support from our specialised external partners for tailored advice and additional assistance.

Moneysmart , opens in new window

Moneysmart is an Australian Government initiative offering free tools, tips and guidance to help you take control of your money.

National Debt Helpline , opens in new window

A not-for-profit service offering free, independent and confidential financial counselling to help you manage debt and get back on track.

Way Forward , opens in new window

A not-for-profit organisation that helps people doing it tough financially to manage and repay debts, especially across multiple banks, by working directly with lenders on your behalf.

Get in touch

Visit a NAB branch

Visit your nearest NAB branch to speak to us in person.

Give us feedback

Suggestions, compliments and complaints.

Request financial hardship assistance online

If you’re having trouble making repayments, you can request assistance via our online form.

Important information

Apologies but the Important Information section you are trying to view is not displaying properly at the moment. Please refresh the page or try again later.